Before we dive in, please be sure to subscribe to the blog page. Also as a reminder, we just launched and created a Facebook page : https://www.facebook.com/CaliforniaSB10

Understanding the Impact of SB 10 on Real Estate Investors, Homebuyers, and Renters

California Senate Bill 10, or SB 10, is another legislative effort aimed at addressing the housing crisis in California. This bill is aimed at allowing more housing developments in areas with high job growth, good schools, and easy access to public transportation.

Here’s what you need to know about SB 10:

Streamlining the Development Process

SB 10 aims to streamline the development process for housing projects by allowing developers to bypass some of the traditional zoning and permitting requirements. This could lead to faster approvals and more streamlined construction timelines, making it easier for developers to build more housing units.

Increased Housing Density

One of the main goals of SB 10 is to increase housing density in areas where job growth and transportation infrastructure are strong. By allowing for more development in these areas, SB 10 could help alleviate the housing shortage and make it easier for renters and homebuyers to find affordable housing.

Opportunities for Real Estate Investors

SB 10 could also present new opportunities for real estate investors looking to capitalize on the increased demand for housing in California. With more development opportunities in high-demand areas, investors could see significant returns on their investment.

Potential Challenges for Existing Homeowners

While SB 10 is aimed at increasing housing density in high-demand areas, it could also present challenges for existing homeowners. The bill allows for the conversion of existing commercial properties into residential properties, which could impact the character of some neighborhoods and increase traffic and congestion in some areas.

Overall, SB 10 has the potential to transform California’s real estate market by increasing housing density in areas with high job growth and good transportation infrastructure. While the bill presents opportunities for real estate investors, it could also present challenges for existing homeowners and neighborhoods. As with any legislative development, it’s important to stay informed about SB 10 and to be prepared to adapt to changes in the real estate market.

In conclusion, SB 9 and SB 10 represent significant legislative developments in California’s real estate market. By increasing development opportunities, streamlining the development process, and addressing the housing crisis, these bills could be game-changers for the industry. Real estate investors, homebuyers, and renters alike should stay informed about these developments and be prepared to capitalize on new opportunities as they arise.

Before we dive in, please be sure to subscribe to the blog page. Also as a reminder, we just launched and created a Facebook page : https://www.facebook.com/CaliforniaSB9

Please like, share, and follow.

How SB 9 Can Help Solve the Housing Crisis and Create Opportunities for first-time Real Estate Investors

California is facing a housing crisis, with skyrocketing prices and a severe shortage of affordable housing. In response to this crisis, the California Senate has passed Senate Bill 9, which could be a game-changer for the real estate market in California. SB 9 allows for the development of two units on most single-family lots, essentially allowing for the creation of up to 4 housing units, (two duplexes) without having to acquire new land.

Here’s what you need to know about SB 9 and how it can benefit you as a real estate investor:

Increased Development Opportunities

SB 9 allows property owners to split their lots into two parcels, allowing for the construction of two separate units. This means that investors can now develop two units on a single-family lot, creating more opportunities for development and profit.

Greater Flexibility for Homeowners

SB 9 also provides greater flexibility for homeowners who are looking to build additional units on their property. Homeowners can now bypass many of the traditional zoning and permit requirements that were previously required, making the process of building additional units much simpler.

Addressing the Housing Crisis

One of the main goals of SB 9 is to address the housing crisis in California. By allowing for the development of two units on a single-family lot, SB 9 creates more opportunities for affordable housing and helps to alleviate the housing shortage.

Potential for Increased Property Values

Finally, SB 9 could potentially increase property values by creating more opportunities for development and making it easier for homeowners to build additional units on their property. This could lead to an overall increase in the value of properties throughout California.

Overall, SB 9 is a promising development for the real estate market in California. By providing increased development opportunities, greater flexibility for homeowners, and addressing the housing crisis, SB 9 could be a game-changer for the real estate industry. As a real estate investor, it’s important to stay informed about developments like these and to be ready to take advantage of new opportunities as they arise.

California Senate Bill 9 (SB 9) provides a unique opportunity for homeowners in California to build wealth and address the state’s housing crisis. By allowing homeowners to split their property into two lots or build up to four units on their existing lot, SB 9 provides increased flexibility in property use and lowers the barrier to entry for homeownership. This can be particularly beneficial for first-time home buyers who may struggle to afford a home in California’s expensive housing market. Additionally, the potential for multigenerational living and the rental income generated from additional units can provide more affordable housing options for families while building wealth through real estate investment. However, it’s important to carefully consider the potential benefits and challenges of SB 9 and work with a trusted real estate professional to make informed decisions. Feel free to contact me anytime with any of your questions: https://gotrealestate.us/contact-me

How California Senate Bill 9 Can Help First-Time Home Buyers Build Wealth and Address the Housing Crisis

Buying a home in California can be a daunting task for first-time home buyers. The high cost of living and limited supply of affordable housing often put the dream of homeownership out of reach for many. However, the recently passed California Senate Bill 9 (SB 9) provides a unique opportunity for first-time home buyers to build wealth and address the state’s housing crisis. Here’s what you need to know:

Increased Flexibility in Property Use

SB 9 allows homeowners to split their property into two lots or build up to four units on their existing lot, providing increased flexibility in property use. This means that homeowners can build additional units on their property and generate rental income, or they can sell one of the lots to help finance their mortgage.

Lower Barrier to Entry for Homeownership

SB 9 provides a lower barrier to entry for homeownership by allowing homeowners to build multiple units on their property. This increases the supply of housing in California, which could help to reduce housing costs over time. Additionally, the rental income generated from additional units could help first-time home buyers to pay off their mortgage faster and build equity in their homes.

Potential for Multigenerational Living

SB 9 also provides opportunities for multigenerational living, which can be a more affordable and sustainable way of living for families. For example, a family could build a duplex on their existing property and live in one unit while renting out the other to family members. This could provide a more affordable housing option for extended families while also building wealth through rental income.

Potential Challenges

While SB 9 provides many potential benefits, there are also potential challenges that need to be considered. For example, building additional units on a property can be costly and time-consuming, which may deter some homeowners. Additionally, some neighborhoods may not be zoned for multiple units, which could limit the availability of this opportunity.

In conclusion

California Senate Bill 9 presents a unique opportunity for first-time home buyers to build wealth and address the state’s housing crisis. The increased flexibility in property use, lower barrier to entry for homeownership, and potential for multigenerational living make SB 9 an attractive option for those looking to buy a home in California. As with any real estate investment, it’s important to carefully consider the potential benefits and challenges of SB 9 and to work with a trusted real estate professional to make informed decisions.

There are two similar bills SB9 and SB10. It is worth to know them both and their unique differences. Please follow my blog page. Click here for Part TWO on SB10 : https://gotrealestate.us/2023/05/07/how-california-senate-bill-10-can-help-address-the-states-housing-crisis

California Senate Bill 10 (SB 10) aims to address the housing crisis in California by streamlining the process for developers to build affordable housing units on underutilized or vacant land. By allowing cities to bypass certain zoning requirements and regulations, SB 10 can expedite the development of much-needed affordable housing units in the state. This can help alleviate the current shortage of affordable housing in California, which has led to skyrocketing housing costs and homelessness. Additionally, the increased availability of affordable housing can benefit individuals and families who struggle to make ends meet in California’s expensive housing market. However, it’s important to carefully consider the potential benefits and challenges of SB 10 and work with a trusted real estate professional to make informed decisions. Please feel free to contact me anytime, I would love to help you and your goals: Click on this link or scan the QR code below: https://gotrealestate.us/contact-me

Contact me

Analyzing the Potential Benefits and Challenges of SB 10 for Californians

The housing crisis in California has been a persistent challenge for policymakers and residents alike. The high cost of living and shortage of affordable housing has led to increased homelessness and displacement, particularly in urban areas. To address these challenges, California Senate Bill 10 (SB 10) was introduced to promote the development of more housing units. Here’s what you need to know about the potential benefits and challenges of SB 10:

Increased Housing Supply

SB 10 aims to increase the supply of housing in California by streamlining the approval process for new housing developments. This could lead to a significant increase in the number of housing units available, making it easier for residents to find affordable housing options.

Addressing the Housing Shortage

California’s housing shortage has been a long-standing challenge, and SB 10 could help to address this issue by allowing for the development of more housing units in high-demand areas. This could be particularly beneficial for low-income residents, who often struggle to find affordable housing.

Encouraging Transit-Oriented Development

SB 10 prioritizes development in areas with good public transportation infrastructure, which could help to reduce reliance on cars and promote more sustainable modes of transportation. This could lead to a reduction in traffic congestion and air pollution, as well as improved accessibility for residents.

Potential Challenges

While SB 10 presents many potential benefits, there are also potential challenges that need to be considered. For example, the bill allows for the conversion of commercial properties into residential units, which could impact the character of some neighborhoods. Additionally, the bill may not be able to fully address the affordable housing crisis, as developers may focus on building more market-rate units instead of affordable housing.

In conclusion,

California Senate Bill 10 has the potential to address the state’s housing crisis by increasing the supply of housing units and promoting transit-oriented development. While the bill presents many potential benefits, there are also potential challenges that need to be addressed. As policymakers and residents work together to address the housing crisis, it’s important to stay informed about legislative developments like SB 10 and to be prepared to adapt to changes in the real estate market.

There are two similar bills SB9 and SB10. It is worth to know them both and their unique differences. Please follow my blog page. Click here for Part ONE on SB9: https://gotrealestate.us/2023/05/07/sb-9-a-game-changer-for-first-time-home-buyers-in-california

As a real estate agent with Coldwell Banker Realty, I’ve seen firsthand the power of homeownership. Despite the initial fear and uncertainty that comes with buying a home, I can confidently say that it’s worth it. In fact, achieving the American dream of homeownership is one of the most important steps you can take toward securing your future.

The Difference Between a House and a Home

There’s a big difference between a house and a home. A house is just a structure – four walls and a roof, maybe a few windows and doors thrown in. But a home? That’s something special. A home is where you make memories, where you feel safe and secure, where you can truly be yourself. A home is where you come back to at the end of a long day, where you relax and unwind, where you spend time with the people you love. A home is where you create your life, and it’s something that no amount of money can buy.

Overcoming the Fear of Commitment

I know that the idea of buying a home can be scary. Maybe you’re worried about taking on too much debt, or maybe you’re not sure if you’re ready for that kind of commitment. But let me tell you something: after the term of the loan, usually 30 years, there is no more payment. That alone is the most significant fact not to mention the tax deductible interest.

Renting might seem like the easy option, but in the long run, it’s only going to hold you back. When you rent, you’re throwing money away on something that will never be yours. You’re at the mercy of your landlord, and you have no control over how much your rent will go up or whether you’ll be able to renew your lease. Buying a home, on the other hand, gives you control over your living situation and allows you to invest in your future.

The Benefits of Homeownership

When you buy a home, you’re not just buying a place to live – you’re investing in your future. Owning a home means building equity, which can help you secure your financial future. And once you’ve paid off your mortgage, you’ll have a valuable asset that you can pass down to your children or use to fund your retirement.

Plus, there are many other benefits to homeownership. For one thing, you can customize your home to your liking, something that’s not possible when you’re renting. You also have more privacy and security when you own a home, and you’re free to make improvements or upgrades that can increase the value of your property. And let’s not forget about the tax deductible interest you can take advantage of.

The Fair Housing Act and the Importance of Fair Housing

The Fair Housing Act was passed on April 11th, 1968, with the aim of eliminating discrimination in housing. While we’ve come a long way since then, there’s still work to be done. As a real estate agent, I’m committed to upholding the principles of fair housing and ensuring that everyone has access to safe, affordable housing.

Whether you’re buying or selling, I’m here to help you navigate the complex world of real estate and make informed decisions that will benefit you and your family. So if you’re thinking about buying a home, don’t let fear hold you back. Remember, achieving the American dream of homeownership is within your reach. With the help of a real estate agent, you can find the perfect home that fits your needs and budget.

One thing to keep in mind is that the home buying process can be complex and confusing, especially for first-time buyers. But don’t worry – that’s why I’m here. As your agent, I’ll guide you through every step of the process, from pre-approval to closing. I’ll help you find the right lender, negotiate the best price, and ensure that you’re getting a fair deal.

Another thing to keep in mind is that buying a home is a long-term commitment. You’ll be responsible for maintaining and repairing your property, paying property taxes, and keeping up with other expenses like utilities and insurance. But despite these responsibilities, owning a home is still one of the best investments you can make.

In conclusion, buying a home is worth it. Not only does it give you a sense of pride and accomplishment, but it also provides long-term financial security and stability. And with the help of a real estate agent, the process can be much easier and less stressful. So if you’re tired of renting and ready to take control of your future, I encourage you to consider homeownership. And as we commemorate the passing of the Fair Housing Act, let’s remember the importance of fair and equitable housing for all.

In the world of real estate financing, knowledge of loans can be the key to unlocking hidden opportunities. One such opportunity is assumable loans. A type of creative financing that not many people are aware of, but can be a game-changer when interest rates hit 6-7%. As a Realtor®, I am a wealth of knowledge and a problem solver, and I am here to share this valuable information with you.

Remember:

“I don’t do loans but I know of them. I am a wealth of knowledge.”

What are Assumable Loans?

Assumable loans are mortgage loans that can be transferred to a new borrower, allowing them to take over the existing mortgage terms and payments. This means that the buyer can assume the seller’s existing mortgage instead of obtaining a new mortgage. This can be beneficial for both buyers and sellers, especially when interest rates begin to rise.

Which Loans are Assumable?

FHA, VA, and USDA loans are all assumable loans. However, the assumability of an FHA loan will depend on the date the loan was issued. FHA loans that were issued before December 1, 1986, are assumable without the need for approval from the FHA or the lender. FHA loans that were issued after December 1, 1986, are assumable, but the buyer must meet certain qualifications and receive approval from the lender. VA loans are generally easier to assume than other types of loans, but the buyer must still meet the VA’s eligibility requirements, and the lender must approve the assumption. USDA loans are also assumable, but the buyer must meet certain qualifications and receive approval from the lender, just like with FHA loans issued after December 1, 1986.

What exactly are FHA Loans?

Now there are several types of FHA loans. The government offers a vast amount of money-saving programs and loans to prospective homebuyers. Here are five common types of FHA loans:

Basic Home Mortgage 203(b)

FHA’s Energy Efficient Mortgage

203(k) Rehab Mortgage

Mortgage Insurance for Disaster Victims Section 203(h)

Assumable loans can be a solution when interest rates hit 6-7%. If the current interest rates are at an all-time high, buyers may be hesitant to make a purchase, as the monthly mortgage payments could be out of their budget. However, with an assumable loan, buyers can assume the seller’s existing mortgage at a much lower interest rate, which means they can purchase the home at a lower cost and save money on interest over the life of the loan. This can make a big difference in their monthly budget and overall financial stability. Additionally, sellers who are looking to sell their home quickly can market their home as an affordable option for buyers, which can increase interest and help the home sell more quickly.

Talk to a Professional

Assumable loans are not widely known, and many people are unaware that this type of creative financing even exists. However, it’s worth exploring this option, especially when interest rates begin to rise. If you’re interested in exploring assumable loans further, it’s worth talking to a professional, such as a real estate agent or a mortgage broker. As a realtor, I am always here to spark a conversation and help you gain trust in the process. I can help you navigate the complexities of creative financing and find the best solution for your unique situation. By taking advantage of assumable loans, you can save money, find affordable housing options, and make the most of your real estate investments.

In conclusion, assumable loans are a hidden secret in real estate financing, but they can be a valuable solution when interest rates hit 6-7%. By assuming an original loan at a low interest rate, buyers can save thousands of dollars over the life of the loan, and sellers can market their homes as affordable options in a competitive market. Don’t miss out on this valuable opportunity – talk to a professional today and explore the benefits of assumable loans!

The Rise and Fall of Silicon Valley Bank: What We Can Learn

Disclosure: As a licensed real estate sales agent and realtor, I must disclose that I don’t have a crystal ball, and I do not know what will happen tomorrow Monday when the stocks open. However, I want to share with you the latest breaking news that Silicon Valley Bank (SVB) has failed.

As a real estate sales agent and a licensed realtor, I would like to begin by disclosing that my expertise lies in the real estate industry. While I strive to provide informed opinions and insights, it is important to note that I do not possess a crystal ball, and I cannot predict what will happen in the stock market or any other industry in the future. As we approach the beginning of the week, I cannot guarantee any specific outcomes or provide investment advice related to the stock market. My focus is solely on the real estate market and providing guidance to those who are looking to buy, sell or invest in properties.

“What I do know is that Real Estate is the best hedge against inflation and uncertainty!” -Jose Cervantes

Silicon Valley Bank (SVB) was once a thriving commercial bank headquartered in Santa Clara, California. It was the largest bank by deposits in Silicon Valley and operated from offices in 13 countries and regions. Unfortunately, on March 10, 2023, it failed after a bank run on its deposits. This news came as a shock to many investors and homebuyers in the area.

The California Department of Financial Protection and Innovation (DFPI) revoked SVB’s charter and transferred the business into receivership under the Federal Deposit Insurance Corporation (FDIC). This marks the second-largest bank failure in U.S. history, and its insured deposits were moved to a new bank created by the FDIC, called the Deposit Insurance National Bank of Santa Clara. According to December 2022 regulatory filings, more than 85% of deposits were uninsured, which means that many customers may lose their money.

Despite this news, there is a silver lining. On March 12, 2023, a joint statement by Secretary of the Treasury Janet L. Yellen, Federal Reserve Chairman Jerome H. Powell, and FDIC Chairman Martin J. Gruenberg stated that all depositors at SVB would be fully protected and have access to all of their money starting the following Monday, March 13. This means that if you were a customer of SVB, you can rest assured that your deposits are safe.

As a licensed real estate sales agent and realtor, I understand that this news may cause some uncertainty for investors and homebuyers in the area. However, I am here to help you navigate the current market conditions and make informed decisions. If you are looking to buy or sell real estate, I am available to discuss your options and help you find the right solution for your needs.

What happened!?

The failure of Silicon Valley Bank (SVB) has sent shockwaves through the banking and tech sectors. The bank failed in a rapid and stunning fashion when customers yanked $42 billion from SVB, leaving the bank with a negative cash balance of $1 billion. SVB and federal regulators could not raise enough capital to make up the difference, and the bank was declared insolvent on Friday. The Federal Deposit Insurance Corp. took control of the bank, and it has promised to pay customers their insured deposits on Monday, but only up to $250,000. The article published by CNN has asked the question, “What’s the next Silicon Valley Bank — and how can the US prevent more chaos?”

When the markets are volatile, and the feds raise rates rapidly, there is a high risk for banks and other financial institutions. This blog will discuss the risks that banks face during market volatility and how to prevent further chaos like SVB’s failure.

The Risks Banks Face During Market Volatility

Banks are at risk of failure during market volatility due to their reliance on short-term funding. During normal times, banks rely on short-term funding to finance their long-term loans. This system works well when interest rates are stable, and liquidity is high. However, during times of market volatility, the opposite is true.

When markets are volatile, interest rates can change rapidly, and banks must scramble to adjust their rates to stay profitable. This can cause a liquidity crunch, where banks have trouble raising the short-term funds they need to continue lending. If banks cannot raise enough capital, they can fail, like SVB.

Another risk for banks during market volatility is the increased likelihood of customer withdrawals. When the market is volatile, customers may panic and withdraw their funds, causing a run on the bank. This can quickly deplete a bank’s cash reserves and cause it to fail.

Finally, banks also face the risk of a loss in value of their investments. During market volatility, the value of stocks and bonds can decline rapidly, causing significant losses for banks that hold these assets. If banks are heavily invested in these assets, they may suffer significant losses, leading to their failure.

How to Prevent Further Chaos Like SVB’s Failure

To prevent further chaos like SVB’s failure, banks must take steps to reduce their risk during times of market volatility. Here are some of the steps banks can take to prevent further chaos:

Diversify their portfolios

Banks must diversify their portfolios to reduce their risk during market volatility. By holding a mix of assets, banks can reduce their exposure to any single asset class. This can help to reduce the impact of any losses on their portfolio.

Manage their liquidity

Banks must manage their liquidity carefully to ensure that they have enough short-term funding to meet their obligations during times of market volatility. This may mean reducing their reliance on short-term funding or holding more cash reserves to weather any liquidity crunches.

Monitor market conditions

Banks must monitor market conditions carefully to stay ahead of any changes in interest rates or other market conditions. This can help them to adjust their rates or portfolios to reduce their risk during times of market volatility.

Work with regulators

Banks must work with regulators to ensure that they are complying with all regulations and best practices. This can help to reduce their risk of failure and prevent further chaos in the financial sector. Fact remains, SVB CEO Greg Becker lobbied the government to relax some Dodd-Frank provisions on regional lenders in 2015. Trump did just that in 2018. https://en.wikipedia.org/wiki/Dodd%E2%80%93Frank_Wall_Street_Reform_and_Consumer_Protection_Act

Educate customers

Banks must educate their customers about the risks of investing and the importance of diversification. By educating their customers, banks can help to prevent panic withdrawals during times of market volatility, reducing their risk of failure. We need more regulation, not less. Bernie was right then, and he is right today, https://www.youtube.com/watch?v=vQE9r5K2oNA

Honestly, I am not sure how all this will play out. The failure of Silicon Valley Bank has highlighted the risks that banks face during market volatility and the unprecedent Fed hikes; increases that had a direct cause of this miscalculation. To prevent further chaos we all must remain calm.

In conclusion, the failure of Silicon Valley Bank may have shocked the financial world, but it is important to remember that every investment carries risks. While no one can predict the future, it is important to stay informed and make informed decisions based on reliable information. As a real estate sales agent, I am here to offer my expertise and help guide you through the process of buying or selling property. Despite the recent events, the real estate market remains strong, and there are still opportunities for those looking to invest. Let’s work together to make your real estate goals a reality.

#California: Are thinking of buying or selling, is so mark your calendar for March 27th!

Remember, I don’t do loan, but I know of them. This announcement is a heads up of a new program available in just a few days. Remember, I am a REALTOR®, a real estate professional. I am here as you resource, when ever you are ready to buy or sell. You can reach me here: Contact me

EXCITING NEWS!

Exciting news for First-Time Homebuyers! In just a few days, on March 27th, the California Housing Finance Agency (CalHFA) is launching a new program called “California Dream For All”. This program is designed to provide up to 20% of the Down Payment and Closing Costs for eligible homebuyers. #CaliforniaDeamForAll #CaDream #AmericanDream Click here for the web site: CalHFA CA DREAM For All.

What sets this program apart from other CalHFA programs is its unique feature of shared appreciation. What this means is that when the home is eventually sold, the initial 20% loan will need to be repaid along with a percentage of the appreciation, which is set at 15% – 20% with a cap of 2.5% of the original amount. Essentially, the shared appreciation feature allows the program to be sustainable over time, so more people can continue to benefit from it in the future. #SharedAppreciation #SharedEquity

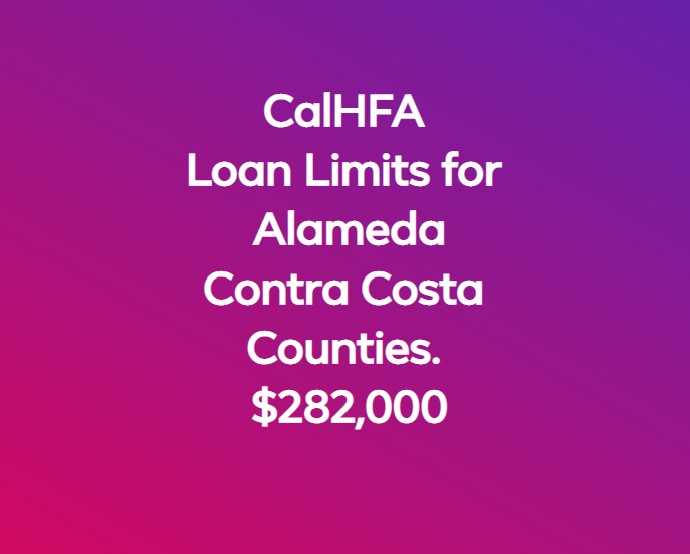

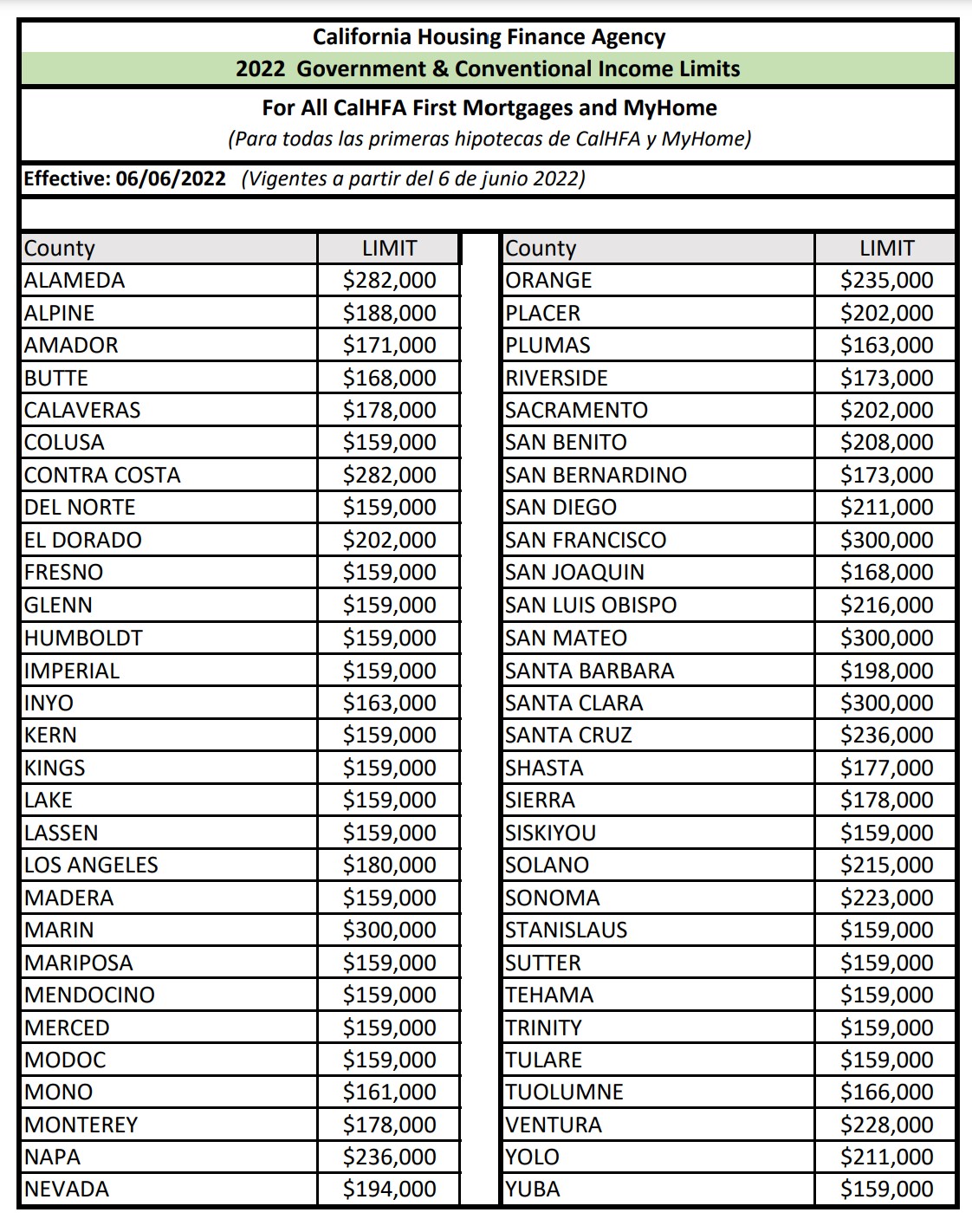

While there are income limits and credit score requirements for the program, they are very generous, making this an excellent opportunity for many individuals and families who may have otherwise struggled to afford a home. The income limits for San Francisco San Mateo Counties for example are $300,000. While across the Bay Area, Alameda and Contra Costa counties loan limits are $282,000. While Sacramento is $202, 000, which is still very generous.

As a seller, this may be the opportunity you’ve been waiting for.

The “California Dream For All” program could be a game-changer for many people, as it offers an incredible chance for homebuyers to get into a new home with much less financial burden. This program could potentially help many families and individuals achieve their dream of homeownership, who may have thought it impossible before. If you’re a first-time homebuyer, be sure to mark your calendar for March 27th and explore this unique opportunity for yourself.

Signup for email updates about the California Dream For All program

www.calhfa.ca.gov

Introduction

The California Housing Finance Agency will be the administrator for the California Dream for All program, as laid out inSenate Bill 197. CalHFA is authorized to provide shared-appreciation loans to help low- and moderate-income first-time homebuyers achieve homeownership. The shared appreciation loans will provide funding to assist with down payments and closing costs.

Current Status

Program Design

The California Housing Finance Agency is currently drafting program terms for the CA Dream for All Program.

There werethree virtual Listening Sessionson September 8, 16 and 20 for interested parties to share their thoughts and suggestions on how the program might be designed to maximize the use of the funds and how to best serve homebuyers.

CA Dream For All” on March 27th, which provides up to 20% of the Down Payment and Closing Costs for eligible homebuyers. With a unique shared appreciation feature, this program offers a sustainable way to help more people achieve their dream of homeownership. Don’t miss out on this excellent opportunity!

As a Realtor®, I understand that buying a property can be an exciting yet overwhelming experience, especially for first-time homebuyers. To help you navigate this process, and give you the facts. Like a myth busters but for real estate. I’ve compiled a list of the top frequently asked questions regarding real estate below.

Should I get pre-qualified before looking for a property?

Yes, it’s highly recommended to get pre-qualified for a mortgage before starting your home search. Pre-qualification provides an estimate of how much you can borrow based on your income, credit score, and other financial factors. This can help you determine your budget and save you time by focusing on homes within your price range.

How much do I need for a down payment on a home?

The amount you need for a down payment will depend on the type of loan you are getting and the lender’s requirements. Generally, conventional loans require a 20% down payment, but there are options for lower down payments, such as FHA loans that require a minimum of 3.5% down payment.

Will I have to pay Private Mortgage Insurance?

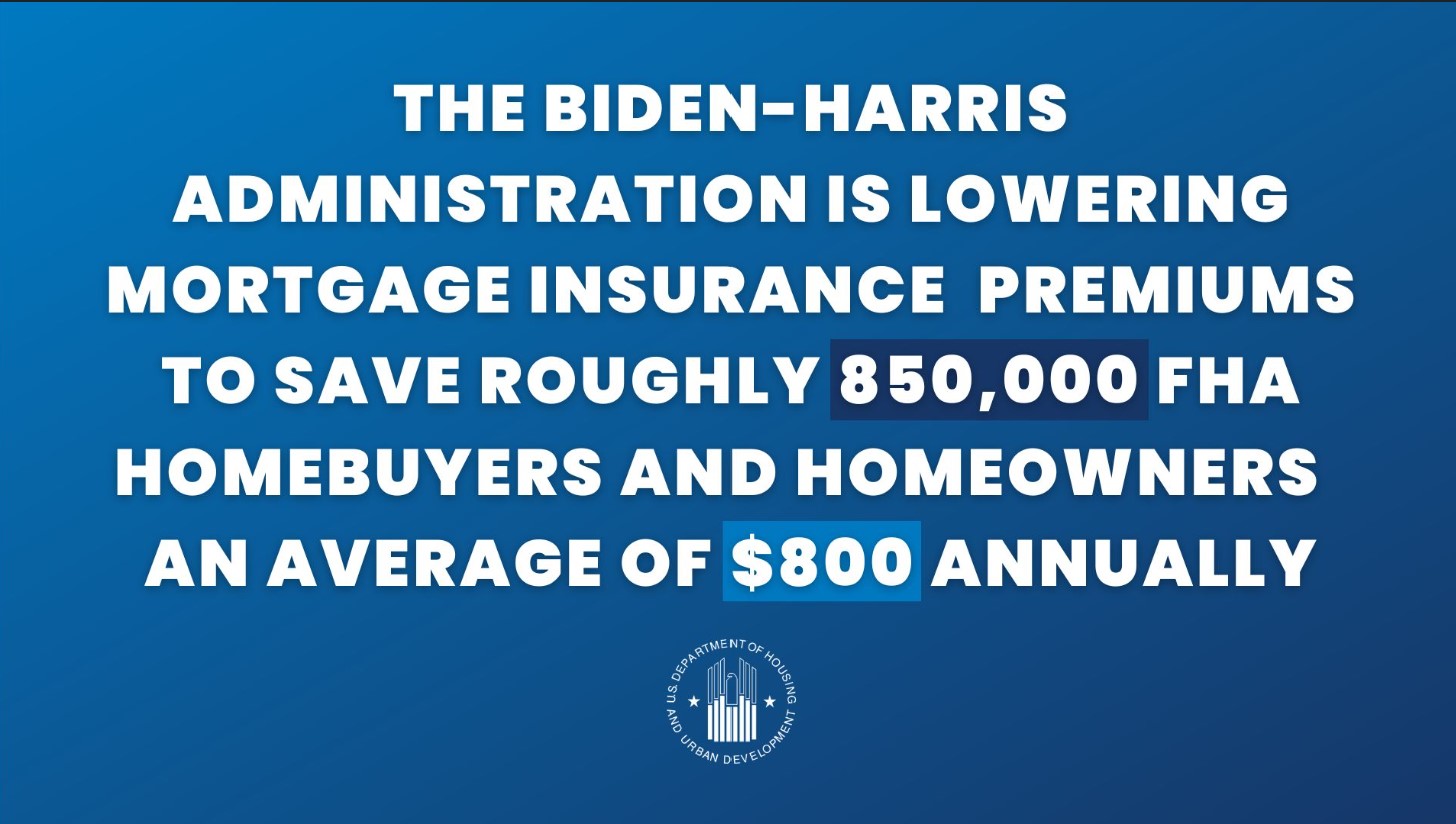

Private Mortgage Insurance (PMI) is required for some types of loans, such as conventional loans with less than 20% down payment. The cost of PMI can vary depending on the loan amount and other factors, but it typically ranges from 0.3% to 1.5% of the loan amount annually. The were recently some great news on this just yesterday from HUD. A “huge” announcement. Link to the press release: https://www.hud.gov/press/press_releases_media_advisories/HUD_No_23_040

Why choose us compared to other?

As a Coldwell Banker Realty agent, I don’t do loans, but I know of them. I am a wealth of information, and provide you with all the options so that you make the most educated and informed decision when it comes to lending. We have access to a vast network of lenders and can help you find the best mortgage option for your needs. We offer personalized service and guidance throughout the homebuying process to help you achieve your homeownership goals.

Do we assist with Commercial properties?

Yes, we have experience and expertise in commercial real estate and can assist you in buying, selling, or leasing commercial properties. In fact as a Coldwell Banker Realty agent, we can help you, locally, nationally, and internationally with your real estate goals.

Is the commission negotiable?

Yes, commission rates are negotiable, and we can discuss this with you during our initial consultation.

Do I qualify for an FHA Loan or any other programs?

There are various mortgage programs available, and we can help you determine if you qualify for an FHA loan or other programs such as VA, USDA, or state-specific programs.

Do you also list Condo properties?

Yes, we can assist you in buying or selling condos, townhouses, and other types of residential properties.

What is the home buying process?

The homebuying process involves several steps, including getting pre-qualified for a mortgage, finding a home, making an offer, getting a home inspection, and closing the deal. As your agent, we will guide you through each step and provide support throughout the process.

How can we meet in person?

We can arrange a meeting at our office, your home, or any other location convenient for you. Alternatively, we can schedule a virtual meeting through video conferencing platforms.

How long does it take to close on a home?

The closing process typically takes 30-45 days, but it can vary depending on the lender’s requirements, appraisal, and other factors. Cash purchase are obviously much quicker and can close in as little as three days.

What is earnest money, and how much is required?

Earnest money is a deposit made by the buyer to demonstrate their commitment to the purchase. The amount required can vary depending on the home’s price and local market conditions, the standard is 3%.

Can I back out of a home purchase contract?

It depends on the terms of the contract and the circumstances of the situation. It’s essential to work with a knowledgeable agent and attorney to understand your options and potential consequences.

How do I know if a property is a good investment?

Various factors can impact a property’s investment potential, including location, condition, market trends, and rental income. A great tool is a CMA, a comparative market analysis, providing you a comparable list of recently sold properties that will help determine the true market value.

What are closing costs, and who pays them?

Closing costs are fees associated with the home purchase transaction, such as appraisal fees, title fees, and insurance fees. These costs are typically paid by the buyer, but some costs can be negotiated between the buyer and seller, depending on the city and county on what is customary.

What is a home inspection, and why is it important?

A home inspection is a thorough examination of the property’s condition, including its structure, systems, and appliances. It’s important to get a home inspection to identify any issues or potential problems with the property before finalizing the purchase.

Can I buy a home with bad credit?

It can be challenging to get a mortgage with bad credit, but there are options available, such as FHA loans, that have more flexible credit requirements.

What is the difference between a real estate agent and a Realtor®?

A real estate agent is licensed to help people buy and sell properties, while a realtor is a member of the National Association of Realtors® and has agreed to abide by a code of ethics and standards of practice. Find out more below is the link to the NAR: Agent vs. REALTOR®

What is a home warranty, and do I need one?

A home warranty is a service contract that covers repairs or replacements of home systems and appliances. Whether you need a home warranty or not depends on your situation and the condition of the home’s systems and appliances.

What happens if my offer is rejected?

If your offer is rejected, you can choose to make a new offer or move on to another property. Your agent can provide guidance on how to proceed based on the seller’s response and market conditions.

In conclusion:

Buying or selling a property can be a complex process, but as your Coldwell Banker Realty agent, I’m here to guide you through each step and answer any questions you may have. Don’t hesitate to reach out to me for any real estate needs. I can send you a free Home Buyer / Seller Handbook. I am a wealth of knowledge here for you. If there is a question you did not read about, please let me know. You can call me, or text me directly with this link: Contact Me!

Remember a great resource and an official website of the United States government:CFPB , the Consumer Financial Protection Bureau, is a 21st century agency that implements and enforces Federal consumer financial law and ensures that markets for consumer financial products are fair, transparent, and competitive.

Elevate Your Space with Matte Wood Finishes and Natural Materials

How to Incorporate Warm Browns into Your Interior Design

The Right Time to Add More Style, Vigor, and Comfort to Your Home

Introduction:

As we move further into 2023, interior design experts predict a shift towards bolder colors, natural materials, and cozy spaces. Whether you’re looking to refresh your home or stage it for sale, incorporating the latest design trends can help elevate your space and make it more inviting. In this blog post, we’ll explore the top interior design trends for 2023, including bold blues, stone slabs, enclosed kitchens, matte wood finishes, natural materials, and warm browns. We’ll also provide tips on how to incorporate these trends into your home for a stylish and comfortable living space.

Bold Blues:

One of the biggest trends for 2023 is the use of bold blues in interior design. From navy to cobalt, deep blue hues can add a touch of elegance and drama to any room. To incorporate this trend into your home, consider painting an accent wall in your living room or bedroom, or add blue throw pillows or a rug to your space. Pairing blue with warm neutrals like beige or taupe can create a cozy and inviting atmosphere.

Stone Slabs:

Another trend that is gaining popularity in 2023 is the use of stone slabs in interior design. From marble to granite, stone slabs can add a luxurious and timeless feel to any space. Consider using a marble slab as a coffee table or kitchen countertop, or incorporating a granite slab as a backsplash in your bathroom or kitchen. The natural texture and veining of stone can add depth and character to your space.

Enclosed Kitchens:

While open-concept kitchens have been popular for several years, enclosed kitchens are making a comeback in 2023. Enclosed kitchens can provide a more intimate and cozy atmosphere, while also allowing for more privacy and noise reduction. Consider installing glass or sliding doors to enclose your kitchen space, or adding a decorative screen or curtain to create a separation between your kitchen and living area.

Matte Wood Finishes:

Matte wood finishes are another trend that is gaining popularity in 2023. Instead of high-gloss or shiny finishes, matte wood finishes can provide a more natural and organic feel to your space. Consider incorporating matte wood finishes in your furniture or flooring, or using a matte finish on your kitchen cabinets or bathroom vanity. Pairing matte wood finishes with warm browns or natural materials like stone or linen can create a cohesive and inviting look.

Natural Materials:

The use of natural materials in interior design is a trend that is here to stay in 2023. From jute to rattan, natural materials can add a sense of warmth and texture to any room. Consider adding a woven rug or pendant light to your space, or using natural materials in your furniture or accessories. Mixing and matching different natural materials can create a layered and eclectic look.

Warm Browns:

Lastly, warm browns are a color trend that is gaining popularity in 2023. From caramel to rust, warm browns can add a cozy and inviting feel to any space. Consider incorporating warm browns in your furniture, accessories, or wall color. Pairing warm browns with natural materials like wood or stone can create a rustic and organic look.

Conclusion:

As we enter 2023, the interior design trends are all about bold colors, natural materials, and cozy spaces. By incorporating the latest trends like bold blues, stone slabs, enclosed kitchens, matte wood finishes, natural materials, and warm browns, you can elevate your space and create a stylish and comfortable living environment. Whether you’re looking to refresh your home or stage it for sale, incorporating these trends can help attract potential buyers and create a lasting impression.

When incorporating these trends, it’s important to keep in mind your personal style and the overall aesthetic of your space. Don’t be afraid to mix and match different trends to create a unique and eclectic look that reflects your personality and taste.

In addition, consider the functionality of your space when incorporating these trends. For example, an enclosed kitchen may not be the best option for those who love to entertain and host dinner parties, while natural materials like jute may not be suitable for those with allergies.

Lastly, don’t overlook the power of lighting and accessories when elevating your space. Adding a statement pendant light or a unique piece of artwork can create a focal point and add visual interest to any room.

In conclusion, the interior design trends for 2023 are all about bold colors, natural materials, and cozy spaces. By incorporating trends like bold blues, stone slabs, enclosed kitchens, matte wood finishes, natural materials, and warm browns, you can create a stylish and comfortable living environment that reflects your personality and taste. So why not take advantage of this opportunity to elevate your space and make it more inviting?

Last but not least, if you are thinking of selling, don’t forget about our RealVitalize program. Look for the blog, and check out my video:

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Understanding the Impact of SB 10 on Real Estate Investors, Homebuyers, and Renters

Understanding the Impact of SB 10 on Real Estate Investors, Homebuyers, and Renters Understanding the Impact of SB 10 on Real Estate Investors, Homebuyers, and Renters

Understanding the Impact of SB 10 on Real Estate Investors, Homebuyers, and Renters

How California Senate Bill 9 Can Help First-Time Home Buyers Build Wealth and Address the Housing Crisis

How California Senate Bill 9 Can Help First-Time Home Buyers Build Wealth and Address the Housing Crisis

The Difference Between a House and a Home

The Difference Between a House and a Home

Plus, there are many other benefits to homeownership. For one thing, you can customize your home to your liking, something that’s not possible when you’re renting. You also have more privacy and security when you own a home, and you’re free to make improvements or upgrades that can increase the value of your property. And let’s not forget about the tax deductible interest you can take advantage of.

Plus, there are many other benefits to homeownership. For one thing, you can customize your home to your liking, something that’s not possible when you’re renting. You also have more privacy and security when you own a home, and you’re free to make improvements or upgrades that can increase the value of your property. And let’s not forget about the tax deductible interest you can take advantage of.

Another thing to keep in mind is that buying a home is a long-term commitment. You’ll be responsible for maintaining and repairing your property, paying property taxes, and keeping up with other expenses like utilities and insurance. But despite these responsibilities, owning a home is still one of the best investments you can make.

Another thing to keep in mind is that buying a home is a long-term commitment. You’ll be responsible for maintaining and repairing your property, paying property taxes, and keeping up with other expenses like utilities and insurance. But despite these responsibilities, owning a home is still one of the best investments you can make.

What are Assumable Loans?

What are Assumable Loans?

Warm Browns:

Warm Browns: