Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

First off, I am not lender.

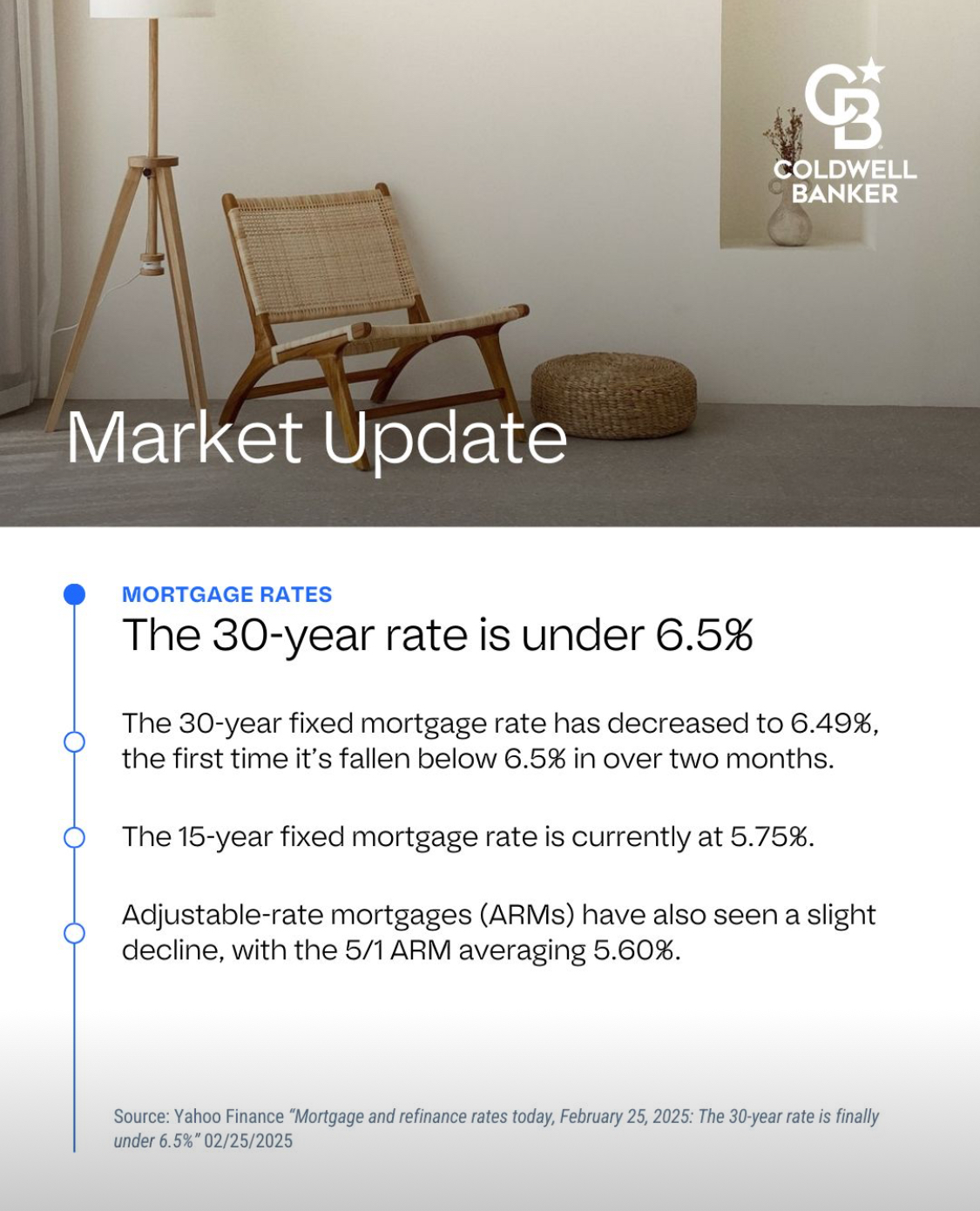

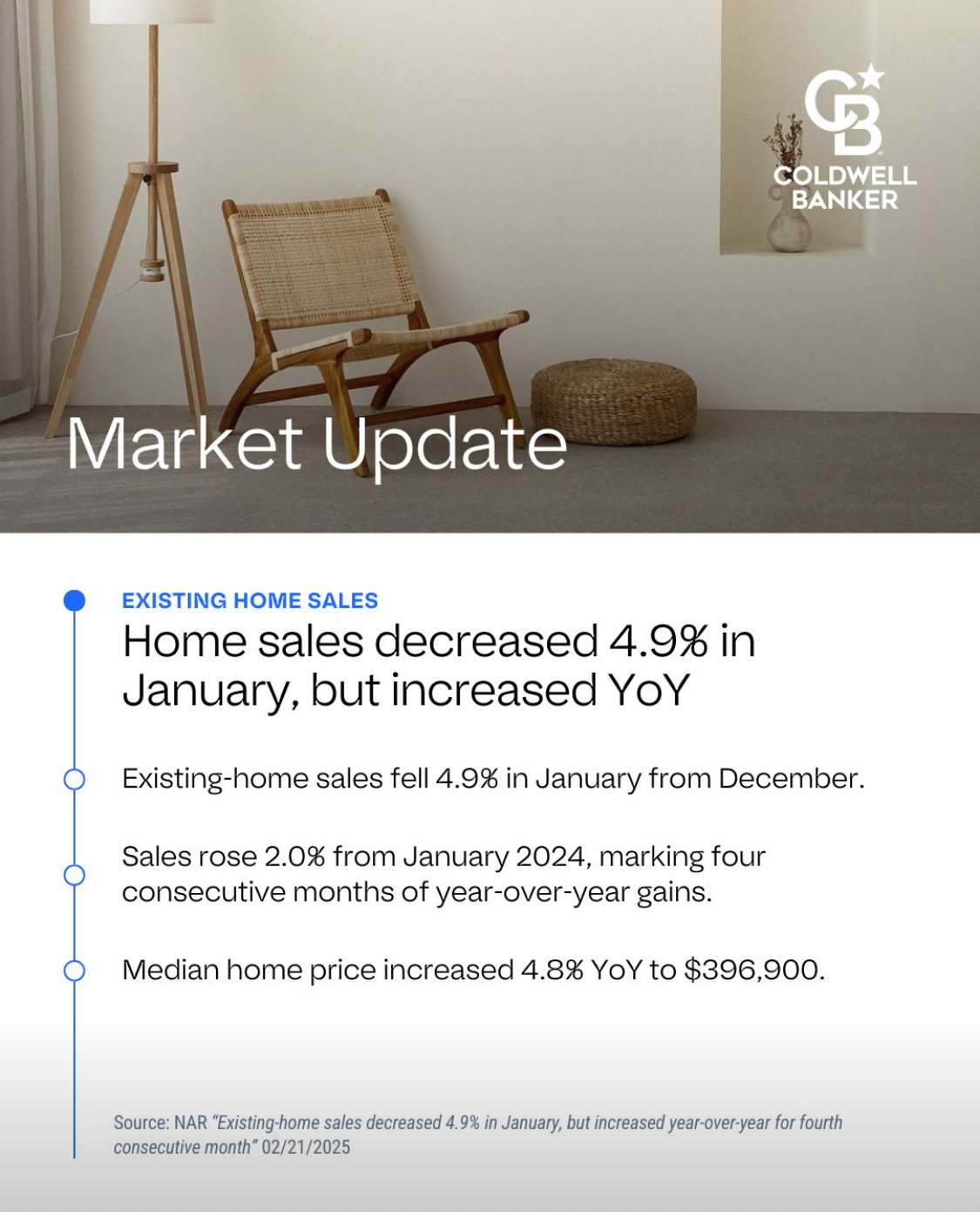

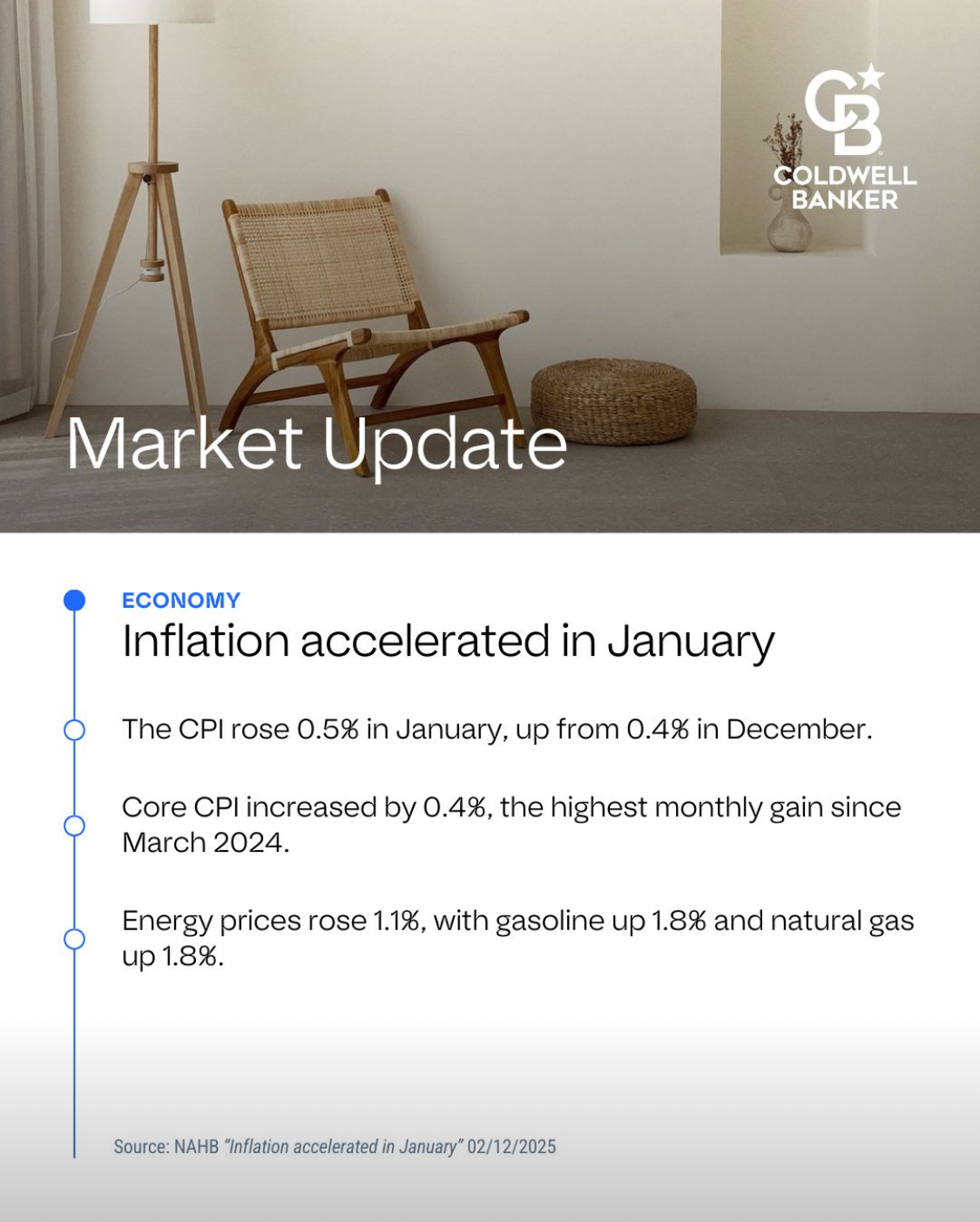

When navigating the home-buying process, especially in today’s market, understanding all your financing options is key to making the best decision for your future. Please note the “Market Update” pages posted on this blog. This may be the perfect storm for many buyers and sellers out there, creating a win win situation. This one strategy may help lower your monthly payments in the early years of your mortgage is a temporary buydown—specifically, a 3-2-1 Buydown.*

What Is a 3-2-1 Buydown?

A 3-2-1 Buydown is a temporary mortgage financing option where the interest rate is reduced for the first three years before adjusting to the full rate for the remainder of the loan. This can significantly ease the burden of high initial mortgage payments. Here’s how it works:

- Year 1: Interest rate is reduced by 3%

- Year 2: Interest rate is reduced by 2%

- Year 3: Interest rate is reduced by 1%

- Year 4 and beyond: The loan returns to the original fixed interest rate

This structure allows buyers to ease into their mortgage payments while potentially growing their income or benefiting from market changes.

Example Calculation of a 3-2-1 Buydown*

Let’s say you’re buying a home with:

- Loan Amount: $500,000

- Fixed Interest Rate: 6.5%

- Loan Term: 30 years

Using a standard mortgage calculator, your payments would look like this:

| Year | Interest Rate | Monthly Payment | Savings Compared to Full Payment |

|---|---|---|---|

| 1 | 3.5% | $2,245 | $743 |

| 2 | 4.5% | $2,533 | $455 |

| 3 | 5.5% | $2,839 | $149 |

| 4-30 | 6.5% | $2,988 | $0 |

Total savings over the first three years: $16,332

2-1 Buydown

Similar to the 3-2-1 but shorter in duration, this option lowers your interest rate:

- 2% below market rate in Year 1

- 1% below market rate in Year 2

- Returns to full rate in Year 3 and beyond

1-0 Buydown

This is a simple one-year reduction:

- 1% lower for Year 1

- Returns to full rate in Year 2 and beyond

Seller-Paid vs. Lender-Paid Buydowns

- Seller-Paid Buydowns: The seller funds the buydown as a closing incentive to attract buyers.

- Lender-Paid Buydowns: The lender covers the buydown in exchange for higher closing costs or a slightly adjusted rate.

Is a 3-2-1 Buydown Right for You?

This financing strategy can be beneficial if:

✅ You expect your income to increase in the next few years.

✅ You want to ease into homeownership with lower initial payments.

✅ You plan to refinance before the higher rate kicks in.

However, it’s crucial to run the numbers with a knowledgeable lender to ensure this aligns with your long-term financial goals.

Who’s Your Realtor?

I am Jose Cervantes, a Realtor with Coldwell Banker Realty—not a lender, but someone who understands how different loan programs can impact your homeownership journey. While Coldwell Banker may have “Banker” in the name, we are a real estate franchise dedicated to helping buyers and sellers maximize their opportunities in the market.

If you’re a seller, we can also help you get top dollar for your home through our exclusive RealVitalize Program, which offers home improvements with no upfront costs.

Why Work with Us?

✅ One-Stop Shop: We connect buyers with trusted lenders, home inspectors, and service providers.

✅ Local & National Reach: Whether buying, selling, or investing, we offer expert guidance at every level.

✅ Peace of Mind: With 21+ years of experience, we provide facts, not fluff, to help you make the best decisions.

Let’s Talk!

Have questions about buydowns, home buying, or selling strategies? Drop a comment below or contact me directly at (650) 200-0852 or (510) 485-3893

Thinking of buying but unsure if you qualify? Let’s explore your options together. Your dream home might be more affordable than you think!

Disclaimer: The 3.5% is possible, but again I am not a lender. I don’t do loans but I know of them. This is for informational purposes only. Interest rates are subject to change and vary based on qualifications. Contact a licensed mortgage professional for current rates and terms.

*Results are hypothetical and may not be accurate. Payment stated does not include taxes and insurance, which will result in a higher payment.

#GotRealEstate